Open Banking Payment Initiation for Billers

Jeroen Dekker

23-09-2021 5m read

Most billers acknowledge that Direct Debit cannot be the only easy way for people to pay their bills. People with irregular and/or low incomes – a growing group - need to manage their finances every month, making the rigidity of Direct Debit a bad it.

Billers might therefore offer cards and wallets as online payment methods in their portal. Those however are very expensive, require complex reconciliation and let customers reverse transactions. Gateways, processors, acquirers, and consumer brands all got rich inserting themselves along the most obvious route for payments: from the consumer’s bank account directly into the biller’s bank account.

Until recently, that direct route required consumers to set up a transfer from scratch in their own banking app. Finding and copying payment details from a sheet of paper or a PDF makes this exercise far from easy: a chore to procrastinate and then forget. Moreover, people can make mistakes, causing exceptions in accounting, negative customer contacts, or even unjustified suspension of service.

Crossing the Chasm: Payment Initiation

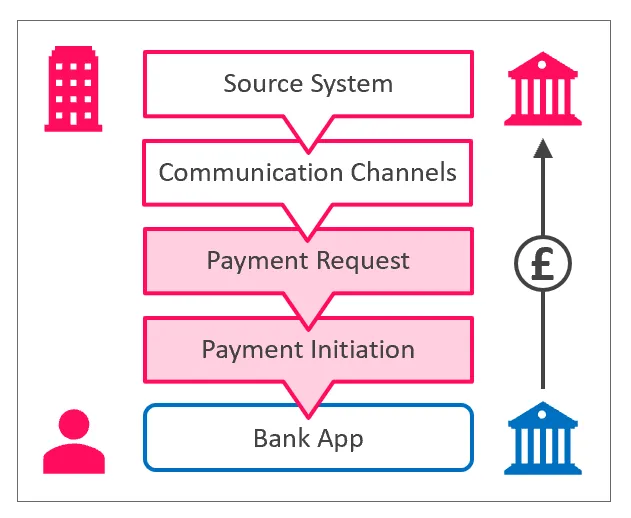

A better way has reached the UK through Open Banking. The banks have published APIs for third parties to – with the consumer’s consent – push the details of a payment straight into the consumer’s chosen bank app for authorization, eliminating the manual retyping. This makes payment easy for the consumer. The result is a UK Faster Payment: cheap (fixed fee), real-time, final, accurate, and a direct 1:1 pay-out that automatically matches the corresponding open item.

The concept is long proven: pushing people to their bank app to authorize a payment is common to payment methods like iDEAL (the Netherlands), EPS (Austria) and POLi (Australia).

The Great Enabler: Payment Requests

But wait, you might say: people don’t pay bills or reminders in a web shop. We need to reach and ask them to pay this bill, that reminder, or a promise-to-pay. How do we ask and enable such payment? From paper, email, SMS, WhatsApp, our portal, our mobile app? How do we introduce this alongside cards and wallets? How do we connect this from our billing and collections systems?

The technical answer to these questions is the Payment Request: a webpage for a specific payment with the details prefilled. Its unique URL can appear as a button, link or QR code in any communication channel. That biller-branded page then hosts Payment Initiation, by itself or alongside cards and wallets. Serrala has implemented its Payment Requests at hundreds of billers in over 20 countries for bill payment, dunning, collection and more. That experience also leads me to the organizational dimension.

Starting the Journey

Payment interactions touch finance, security, compliance, IT, privacy, customer experience, communications… where do we begin, who owns it, how do we make it work with our processes, educate our customers? Having crossed these hurdles many times, recent conversations with UK billers looking to adopt Payment Initiation surfaced a tendency to fear the leap. “Take a step back, rethink our customer journeys, assess the IT side of things… there shall be an Internal Project.” All valid thoughts, as introducing this innovation affects two keystones of any business: customers and cash. But why reinvent the wheel yourself? A specialized vendor brings more than software: it can provide practical implementation expertise to expedite your journey from blank slate to live use cases. Give them a seat at your table: the benefits of Payment Initiation await.

Download Whitepaper

For further details on the new solution and our channel partnership with Tink, please go to the whitepaper.